In almost every way measurable, millennials in the U.S. at 40 are doing worse financially than the generations that came before them.

Fewer millennials own homes than their parents did at their age. They have more debt — especially student debt. They simply aren’t as wealthy.

Now, if predictions of a long, post-Covid economic boom are to be believed, this may be the last opportunity an entire generation has to build wealth before heading off into retirement.

For Kellie Beach, a real-estate attorney who turned 40 in April, that means starting by aggressively paying down her credit-card debt. Beach has cycled between periods of carrying balances and paying it all off. “I stayed afloat with credit cards,” she said. “I was just used to swiping and overspending.”

The pandemic jolted her into taking a hard look at her habits.

“Now I have this feeling — like this fire — of urgency,” Beach said. “I’m not going to be in this place again. I can’t wait to get out of this debt. I can’t wait to save up for my emergency fund and invest again.”

Amazon said Wednesday it will acquire MGM Studios for $8.45 billion, marking its boldest move yet into the entertainment industry and turbocharging its streaming ambitions.

The deal is the second-largest acquisition in Amazon’s history, behind its $13.7 billion purchase of Whole Foods in 2017.

Amazon said it hopes to leverage MGM’s storied filmmaking history and wide-ranging catalog of 4,000 films and 17,000 TV shows to help bolster Amazon Studios, its film, and TV division.

“The real financial value behind this deal is the treasure trove of IP in the deep catalog that we plan to reimagine and develop together with MGM’s talented team,” said Mike Hopkins, senior vice president of Prime Video and Amazon Studios. “It’s very exciting and provides so many opportunities for high-quality storytelling.”

In a statement, MGM Chairman Kevin Ulrich said: “The opportunity to align MGM’s storied history with Amazon is an inspiring combination.”

Shares of Amazon barely moved on the announcement.

Over the last 15 years, I whittled down close to six figures of debt I acquired from living beyond my means. In that time, I alternated between ignoring it, agonizing over it, and finally, taking action; I became debt-free last year. Along the way, I read lots of books about money. Since April is National Financial Literacy Month, I wanted to share these nine books about personal finance that each taught me something valuable about managing my money.

The first few are more about the emotional aspects of money, which is where I faced my biggest financial stumbling blocks, while others get into the nitty-gritty of managing your money. I haven’t followed any single book to the letter, which would be impossible since some give contradictory advice. I also don’t necessarily agree with everything each of these authors writes. I have, however, gained the confidence and knowledge I’m using to keep my finances on an upward trajectory. I also learned what doesn’t work for me. I know reading any single book can’t make money simply appear in your bank account (though wouldn’t that be wonderful?), but diving into the topic helped me grapple with the ways I treated money that I wanted to change.

Her mom grew up on a wheat farm, and for years, the government had been paying her family $15,000 a year to not farm. It was an attempt to keep land from being overused, and that money was basically the extent of Megan’s relationship with agriculture: the source of a yearly gift, the money she and her mom would wait for before, say, buying furniture or making home repairs. Now Megan, who asked to be referred to by a pseudonym to speak freely about her finances, receives that money directly.

In 2019, at the age of 64, Megan’s mother died. It was expected and unexpected. Her mom had been a cancer survivor for 20 years. But chemotherapy had damaged her heart, and two years ago, she went into cardiac arrest.

On the phone, Megan, 38, runs me through the process of settling her mother’s estate. It was a ton of bureaucracy: so many phone calls, so much paperwork. After paying her mom’s bills and taxes, selling off her house and possessions, and handling lawyers’ fees — setting aside for just a second the small piece of land that makes her an agricultural scion — it came to just under $50,000.

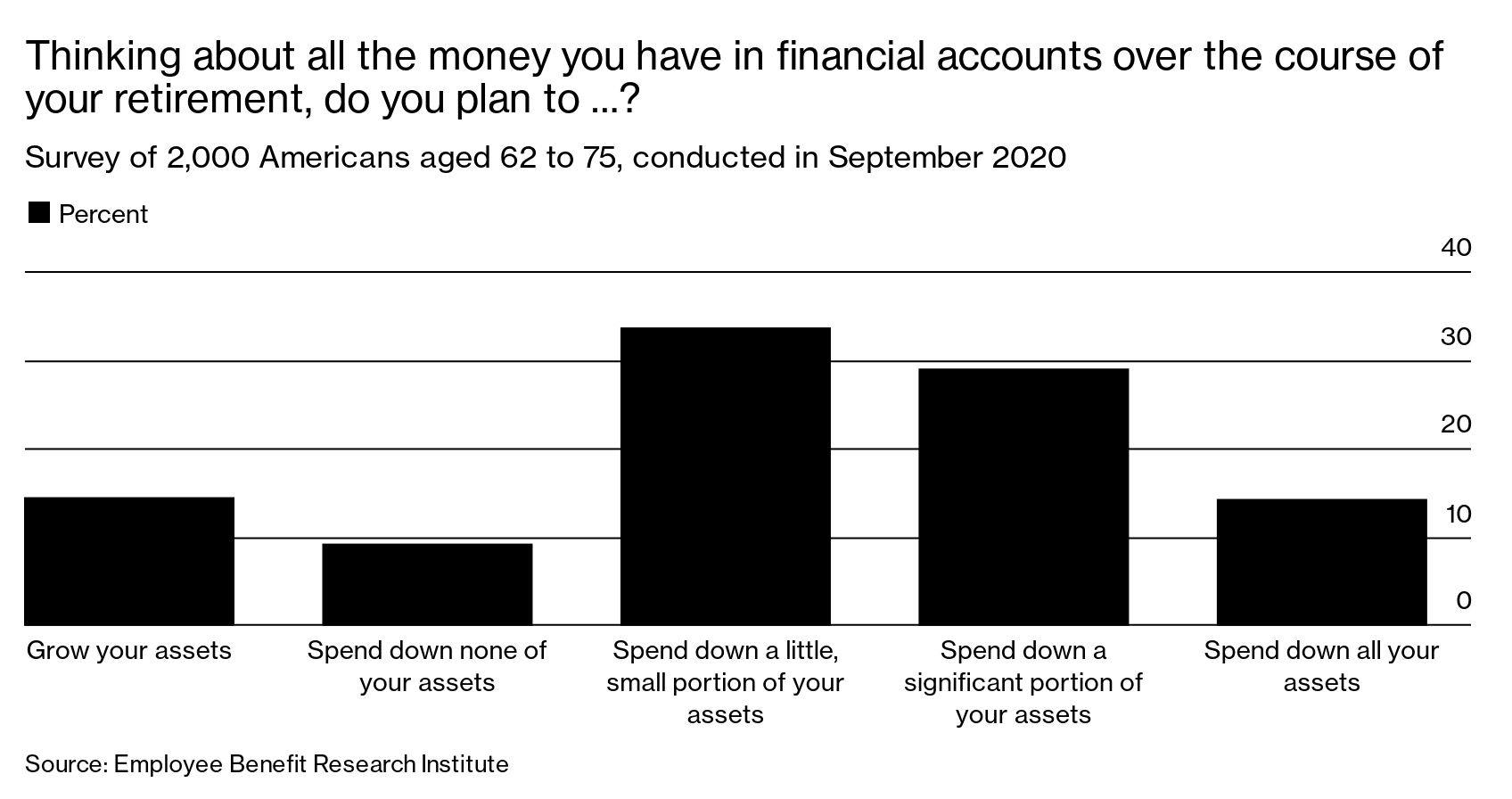

There’s a school of thought that you should spend down all your assets in retirement and “bounce the check to the undertaker,” as Michael Bloomberg, founder and majority owner of Bloomberg LP, our publisher, likes to say. But not many Americans subscribe to that school of thought. A fascinating survey from the Employee Benefit Research Institute explores how people feel about spending in retirement. It doesn’t fit with finance theory. “There’s just something we’re not getting quite right in understanding how people navigate retirement,” Lori Lucas, the president, and chief executive officer of EBRI, said March 24 in announcing the results.

As this first chart shows, only 14.1% of respondents think they’ll spend down all their assets. If you add up the three left-most columns, 57% plan to grow their assets in retirement, leave them untouched, or spend down only a little. The survey by EBRI, a nonprofit research group, was conducted in September and covered 2,000 Americans ages 62 to 75, 97% of whom were retired. So U.S. undertakers don’t need to fear bounced checks.

The golden years can offer great promise — moments with grandchildren, time for travel and leisure. But they can also be a source of great stress — over money, declining health, and decisions about relocation.

Where you retire can make all the difference. A recent study by the financial website WalletHub.com offers some guidance, ranking each of the 50 states in terms of their suitability for retirement. A total of 45 metrics across three categories (affordability, quality of life, and health care) were weighed to rate every state.

Among the measures of affordability were the cost of living, annual costs of adult day care and in-home services, taxes, and inheritance laws.

Each state’s health care rating was affected by the quality and availability of geriatric care, the life expectancy and health of seniors, and even Covid-19 positivity and death rates — good to know for this pandemic or the next — among other factors.

Typically, investors make most of their money in the stock market by selling shares at a profit. But by purchasing shares of dividend-paying stocks, you can get rewarded regularly for holding onto those shares.

Companies pay their investors dividends based on the number of shares they own. If, for example, a company distributes an annual dividend of $2 per share and you own 1,000 shares, you’ll qualify for $2,000 in dividends as long as you’ve met the holding period requirements.

Typically, dividends are paid quarterly, though a small minority of companies distribute them on other schedules. Each time the board of directors declares a dividend, you will receive deposits in your account. And if a company increases its dividend payout — which some have a habit of doing at least once a year — you’ll get those “pay raises” without having to do anything extra at all.

Film and Writing Festival for Comedy. Showcasing best of comedy short films at the FEEDBACK Film Festival. Plus, showcasing best of comedy novels, short stories, poems, screenplays (TV, short, feature) at the festival performed by professional actors.

.

.

.

.

.

.

.

.